19 years of data. One clear conclusion. The infrastructure layer is missing.

Date

09.06.26

Author

Vishal Bhatia | Executive Director

When we acquired Angels Den six months ago, we expected to find a platform with untapped potential and a few operational gaps.

What we found was a nineteen-year data set sitting largely unread.

We have spent the last six months reading it properly.

This is what it says.

The Numbers

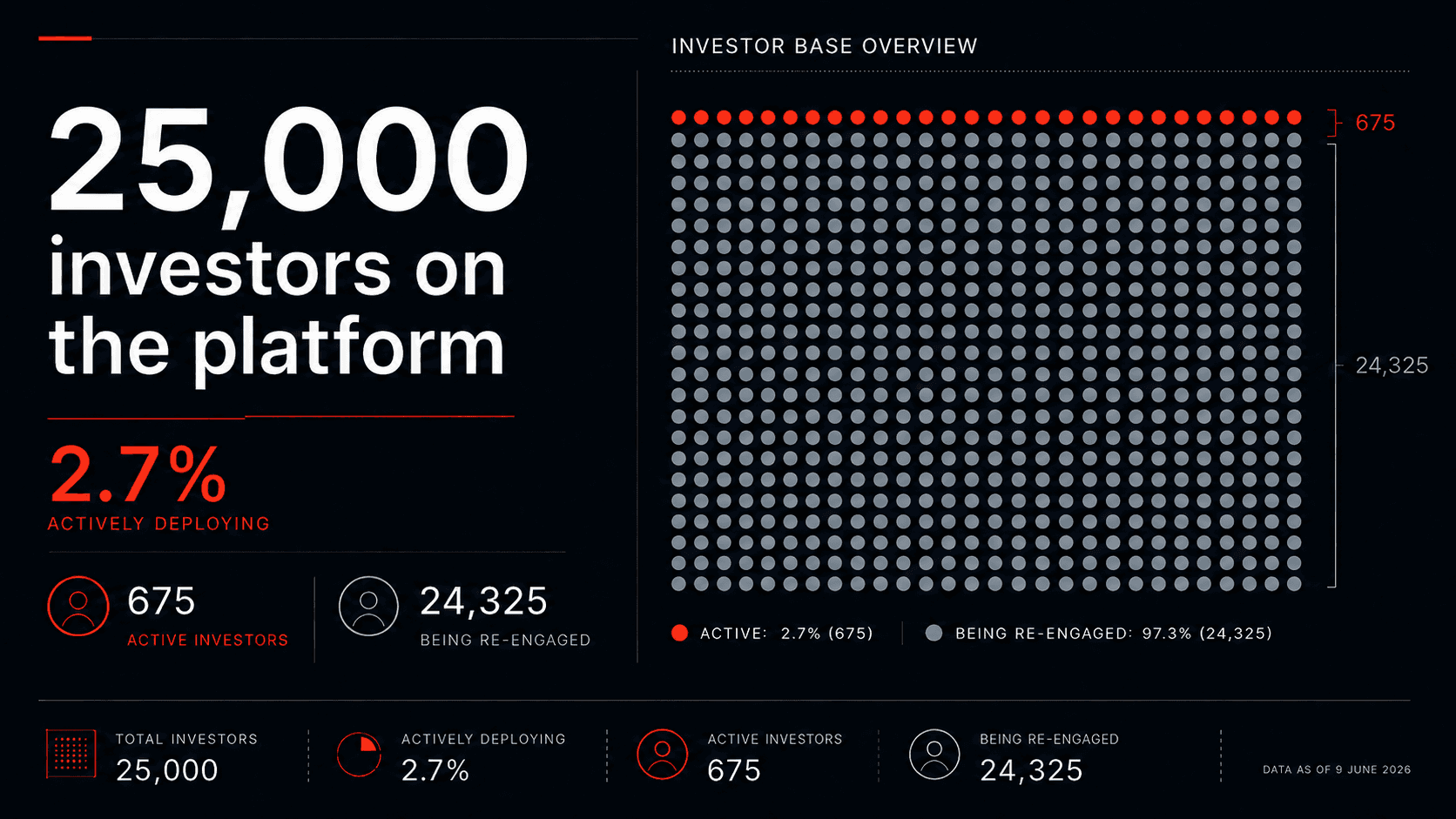

There are over 25,000 investors registered on the Angels Den platform.

Less than 2.7% are actively deploying right now.

That is not a market problem. That is a relationship problem. Thousands of investors have sat on this platform for years without a single meaningful conversation. We are working through them one by one. It is slow. It is necessary. It is working.

On the founder side, the picture is just as revealing.

Since our new site launched in January, over 2,000 pitches have come through the platform. Around 12% are selected.

Most people hear that and assume the bar is too high.

We think the bar is exactly right. The real question is what sits behind the 88% that do not make it through.

What Is Actually Killing Deals

It is not bad ideas.

It is not a lack of ambition.

It is almost always the same short list of failures, repeated across hundreds of submissions.

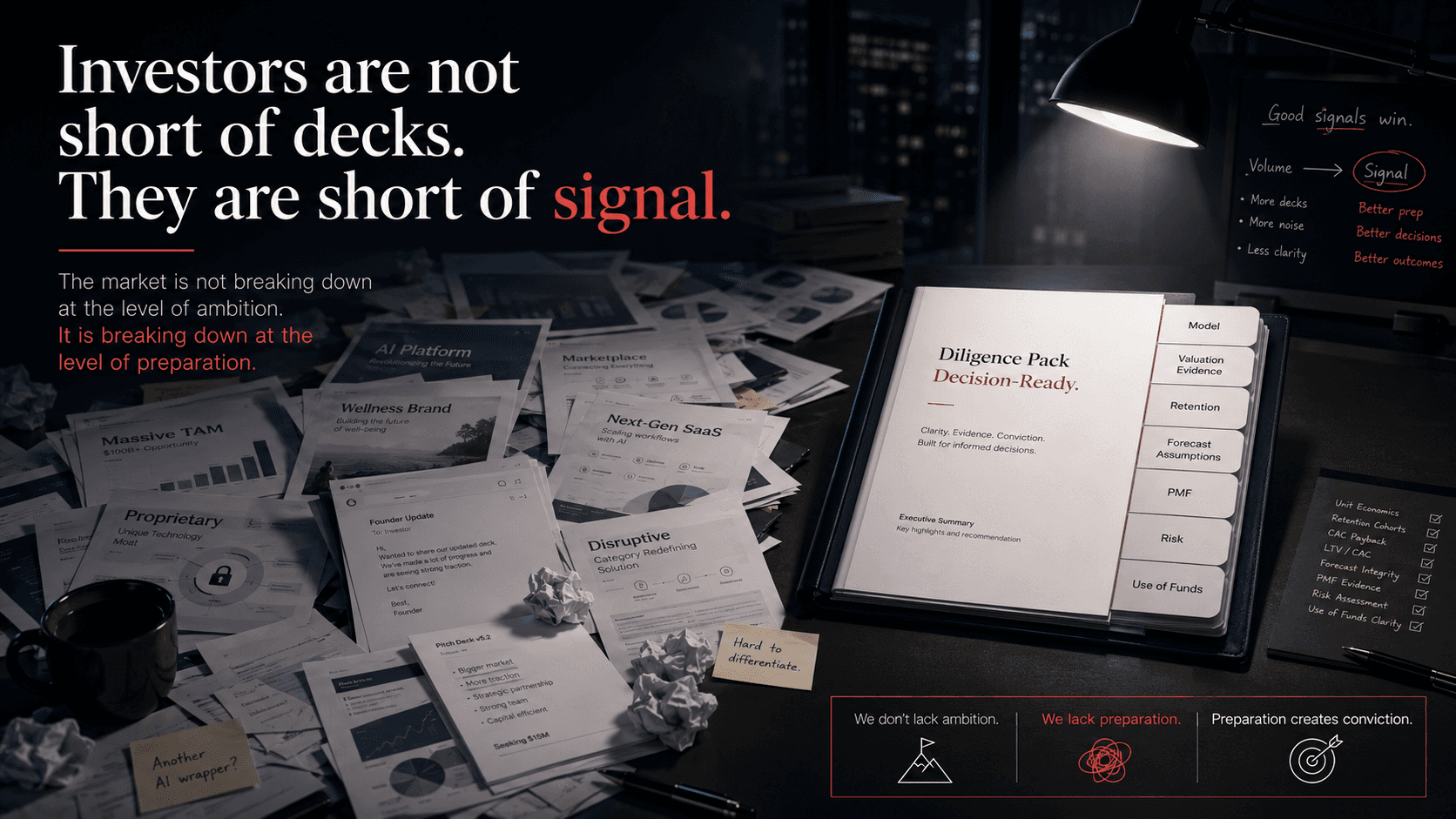

Founders who cannot talk through their unit economics without pulling up a document. No data room, or a data room that is just a deck with a different label. Financials with no assumptions underneath them. Defensibility described in adjectives: proprietary, differentiated, first-mover. Nothing behind the words.

Then there is the concentration problem.

In any given week, we see five or six pitches solving the same problem in almost the same way. The same AI workflow tools. The same crowded marketplace plays. The same wellness brands differentiated mainly by packaging.

Founders are reading the same signals, drawing the same conclusions and arriving with different versions of the same company.

This is not a failure of creativity. It is structural. The cost of launching has collapsed, the cost of raising has not. That gap is widening and most founders have not adjusted to it.

What Investors Are Actually Saying

The investors who are deploying are not telling us there is no appetite.

They are telling us there is no signal.

They are not short of decks, they are short of prepared opportunities.

They are not asking for perfection, they are asking for the basics to be clear enough to make a decision.

What is the model? What evidence supports the valuation? What does retention actually look like? What assumptions sit underneath the forecast? What has to be true for this business to become materially valuable?

Too often, investors are doing forensic work just to decide whether something is worth proper diligence. That is where the market is breaking down. Not at the level of ambition but at the level of preparation.

The Real Diagnosis

We keep arriving at the same uncomfortable conclusion.

The UK early-stage market does not have a capital problem. It has an infrastructure problem.

There is angel capital, there is founder ambition and there are genuinely good companies being built. What is missing is the layer between them: the preparation standards, the diligence scaffolding, the curation infrastructure that lets a serious investor evaluate a serious opportunity without spending half a week working out whether the basics are even in place.

That infrastructure layer exists in later-stage markets. Series A and beyond has process, it has expectations and it has frameworks both sides understand before they enter the room.

Early-stage does not.

Founders arrive before they are ready, Investors wade through volume looking for signal. Platforms have optimised for pitch flow over investability. The result is a market that looks busy but does not function well. Lots of activity, fewer decisions, lots of conversations, slower rounds. Capital that exists in theory but moves too slowly in practice.

This is not a cyclical problem, it is a structural one and it will not fix itself.

What The Infrastructure Layer Actually Needs To Do

When we talk about infrastructure at early stage, we mean something specific.

It means preparation standards that founders are held to before they reach investors, not after. Clear expectations around data rooms, financial assumptions, evidence of product-market fit and defensibility in specifics rather than adjectives.

It means curation with a real filter, not a light one. Fewer opportunities presented with genuine conviction rather than more opportunities presented with caveats.

It means diligence processes that compress time rather than extend it. The average early-stage round in the UK takes far longer than it should, not because the analysis is complicated but because nobody has built the scaffolding to make it efficient.

It means investor networks designed around deployment, not registration. A platform with 25,000 names means nothing if 97% of them are not active. What matters is the quality and engagement of the network, not its size on paper.

And it means feedback that actually flows. Right now, founders do not know what investors need until they are already in the room. Investors do not communicate what would move them to yes. Both sides are operating with incomplete information and paying for it in wasted time and lost deals.

Why Capital Is Moving Too Slowly

This comes up from both sides of the table, consistently.

Founders wait months for decisions that should take weeks. Investors hesitate on opportunities they should be able to evaluate in days. Rounds drift. Momentum dies. Businesses that should be funded either close down their rounds or quietly disappear.

It would be easy to blame market conditions. That is too convenient.

The real problem runs in both directions. Founders do not always understand what investors need in order to say yes, they send decks instead of building diligence packs. They answer the question that was asked instead of the concern underneath it, they confuse storytelling with substance.

Investors, in turn, do not always communicate what would actually move them. They ask for more information without specifying what, they defer when a focused conversation would resolve the issue, they expect founders to anticipate requirements that have never been properly articulated.

The result is a slow, foggy and expensive process for everyone.

What We Are Building

Angels Den sits at an unusual point in this market. Nineteen years of history. A platform with scale. Visibility across thousands of founder and investor interactions simultaneously.

That position comes with a responsibility we take seriously: to raise the standard of what early-stage investing looks like in the UK, not just to process more of the same.

We are reworking selection around investment readiness rather than novelty. A pitch arriving at Angels Den now has to clear a meaningful bar before it reaches investors: a proper data room, clear financials with assumptions, evidence of product-market fit beyond anecdote, defensibility in specifics. We would rather present fewer opportunities with confidence than more with caveats.

On the investor side, we are moving away from the legacy model that incentivised volume over quality on both ends. We are building a curated membership network designed around active deployment: founding members, tiered access, micro-syndicate structures. Built for investors who actually write cheques, not just the long tail of names who watch.

We are also introducing new formats that compress the diligence process itself. DDQ Hot Rooms bring a small group of active investors into a structured session with a single founder, designed to surface the real questions and move serious conversations to decisions faster, not a pitch event with a different name. A working process built around the infrastructure gap we have identified.

Alongside this, we are rolling out DDQ preparation and reporting for founders before they enter any investor conversation. The goal is not to coach founders to perform, it is to make sure they are genuinely investment-ready in the way active investors actually need them to be.

What Comes Next

Over the coming months, we will share more of what the data is telling us.

Sector concentration. How investors say they make decisions versus how they actually make them. The specific gaps between what founders submit and what investors need to see, some of it will be uncomfortable reading for parts of the ecosystem.

That is the point.

The early-stage market does not need more pitch events, it does not need more platforms optimising for volume, it needs preparation infrastructure, diligence standards and faster paths to conviction on both sides of the table.

That is what we are building.

Founders who want to be considered for our first DDQ Hot Rooms, and investors who want a seat in the room, can register interest through our website now.

Six months in, the diagnosis is clear.

The work starts here.